Wednesday 3rd April 2013. Stock index and index futures regain positive momentum yesterday after coming down for some retracement last three sessions. Other news to follow.

"-- U.S. stocks gained Tuesday, with the Dow Jones Industrial Average DJIA +0.61% and the S&P 500SPX +0.52% both closing at record highs as health insurers rallied on Medicare-reimbursement news and U.S. factory orders rose in February. The Dow industrials rose 88.16 points, or 0.6%, to 14,662.01, with the blue-chip index topping the prior record hit late last week. The S&P 500 added 8.08 points, or 0.5%, to 1,570.25, its all-time closing high. The Nasdaq Composite COMP +0.48% rose 15.69 points, or 0.5%, to end at 3,254.86, with the technology-heavy index 1,793.76 points from its record-high finish of 5,048.62, set on March 10, 2000."

"Asian stocks generally fell on Tuesday, as a stronger yen weighed on the Japanese market, while the Reserve Bank of Australia’s decision to keep interest rates unchanged lifted the Sydney market. Japan’s Nikkei Stock Average lost 1.1% after dropping by as much as 2.7% in early trading, falling to its lowest level since March 6 amid a stronger yen. Among the key regional markets, Japan's Nikkei 225 fell 1.08% to 12,003.43; Shanghai's Composite Index shed 0.30% to 2,227.74 and South Korea's Kospi lost 0.49% to 1,986.15. Singapore's Straits Times Index inched up 0.3% to 3,317.59; Hong Kong's Hang Seng Index rose 0.31% to 22,367.82 and Taiwan's Taiex gained 0.18% to 7,913.18. At Bursa Malaysia, blue chips rallied on strong fund buying of index-linked stocks which also saw the spillover of interest to second liners."

"- Oil futures logged a slight gain , recouping most of the previous session's loss. Weak manufacturing data from Europe and the U.S. pressured prices early on, but traders factored in uncertainty ahead of U.S. petroleum supply data and nonfarm payrolls report. May crudeCLK3 -0.51% rose 12 cents, or 0.1%, to settle at $97.19 a barrel on the New York Mercantile Exchange, after losing 0.2% on Monday."

"-May Soybeans finished up 3 1/4 at 1394, 11 3/4 off the high and 8 up from the low. July Soybeans closed up 2 1/4 at 1374 1/2. This was 7 3/4 up from the low and 11 1/2 off the high.

FKLI- Bulls Are Still Controlling The Tempo

After losing some points to the Bears for the past three sessions, Bulls came back to action yesterday by pushing the index up and they did it with flying colours. The market ended in strong note with April contract topped out 10 weeks high around 1,686 level while FBM KLCI ended higher to 1,685 level. Strong Buying interest by foreign fund help support the rallies as local stock market may be shielded from external shocks such as financial set back on European Union but the condition is gradually improving. Reuters reported European shares extended gains on Tuesday when new data showed the region's factory activity no worse than originally estimated in March, while the euro slipped as investors worried about the impact of the Cyprus bailout. Technically, the spot month contract is likely coming out from correction phase after rallying to a new weekly high yesterday. As mentioned on previous post, past retracement was deem typical or normal sight in any form of uptrend. Market have to retrace and correct for profit taking activities and then rally back when it appear appealing to attract Buyers again. The old news regarding parliament dissolution may not the headlines for the market to move at the moment unless there is any official announcement made by the government officials. So far, there was little development on the Malaysia general election date but almost everyday you can hear most political party is gearing up for the upcoming 13th general election. This week, pivot support is located around 1,665 followed by 1,650 while resistance is pegged at 1700.

P/s: KUALA LUMPUR: Cameramen and journalists have been waiting at the gates of Istana Negara since 7am Wednesday in anticipation of an announcement of the general election. - The Star

Daily Pivot Point

R2= 1700

R1= 1690

S1= 1665

S2= 1650

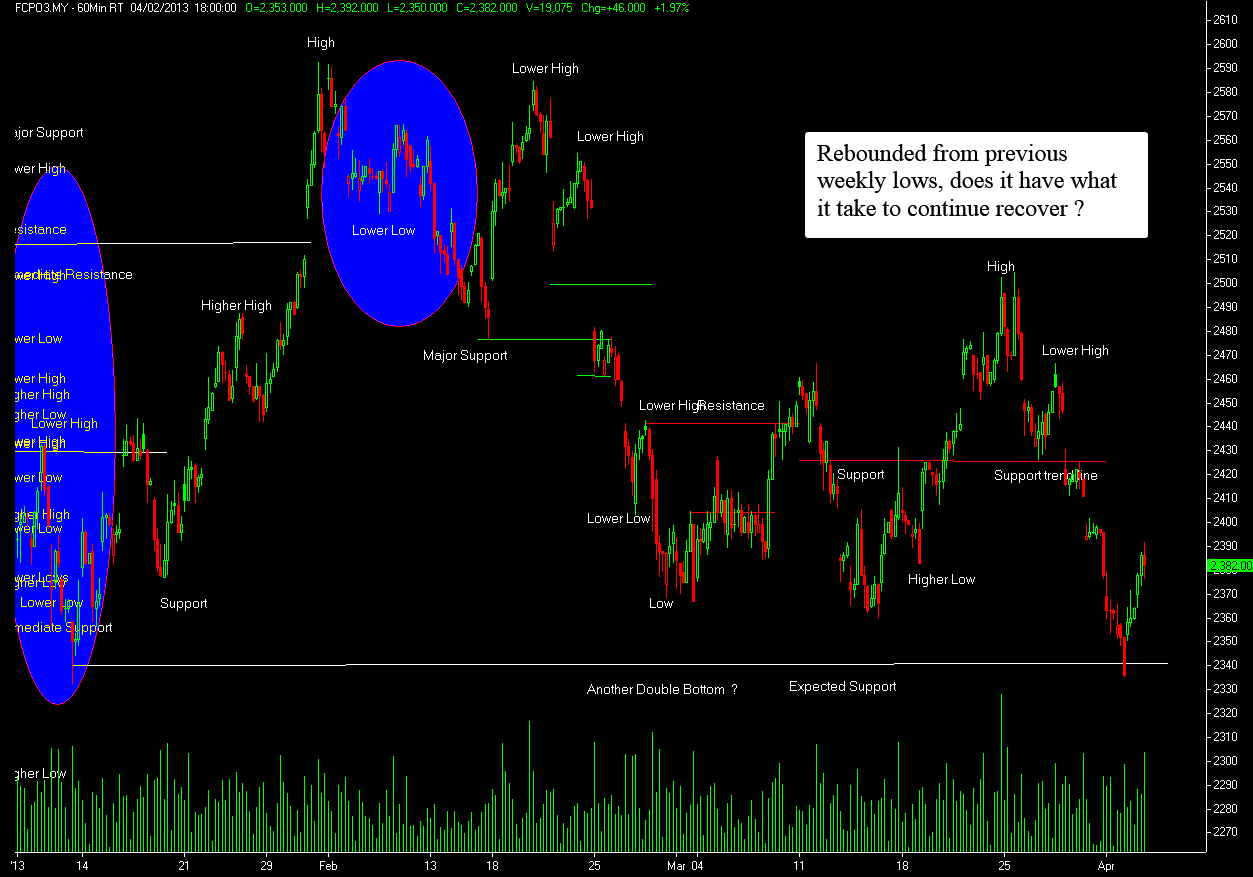

FCPO- Technical Rebound On Temporary Double Bottom

Market went up yesterday amid recent slightly positive export data announce on last Monday this week. Market participants are expecting lower export figures but the actual export data made yesterday rallies possible. Increased exports will help trim down record high stocks gradually, and this is a good news for the market to recover slowly. Technically, the benchmark Jun manage to rallied about 1.9% higher to 2,382 level yesterday after it went down to 2,335 level, which appear to be previous major weekly support area. It is good for the benchmark Jun to recovered but not still not good enough to confirm any medium term upside based on this double bottom candle pattern seen on daily chart. The 1.9% came short to make this rally an reliable signal to go Long on medium term as it has to sustain at least 2% rally on the close. Else it would turn out to be another temporary or technical rally. For today, the benchmark Jun is likely open lower and heading down gradually amid weak overnight correction made on Soy oil. Soy products had came down due to surprise increased on stockpiles reported on USDA last Thursday. This week, the benchmark Jun contract trading range for pivot point support is likely located around 2,357 followed by 2,332 while resistance is pegged at 2,416.

Daily Pivot Point

R2= 2416

R1= 2399

S1= 2357

S2= 2332

Disclaimer: Information and opinions contained in this report are for educational purposes only. While the information contained herein was obtained from sources believed to be reliable, author does not guarantee its accuracy or completeness.

0 comments:

Post a Comment